{kind=link}

Fiscal Progressivity

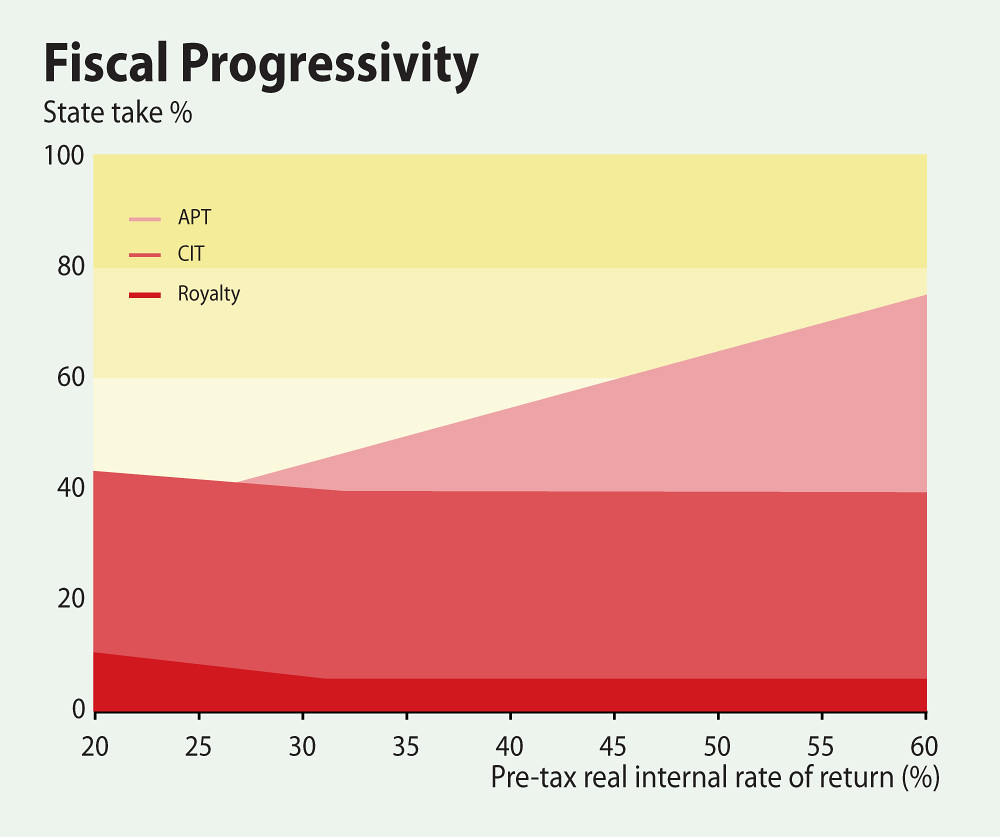

This figure shows the contribution of three different fiscal elements to the fiscal burden on a mining project: corporate income tax, additional profits tax, and royalty. The burden is measured in terms of state take (y-axis) at progressively higher levels of project profitability on a pre-tax basis (x-axis). Whereas the combination of royalty (at 5 per cent) and income tax (at 35 per cent) results in a state take of close to 40 per cent, the additional profits tax is triggered in stages to achieve a higher level of state take as project profitability increases. (APT – additional profits tax; CIT - corporate income tax; IRR – internal rate of return).

Year: 2014

From collection: Deep Sea Minerals Volume 2

Cartographer: GRID-Arendal